Real estate tax strategies are often a key part of the conversation for property owners and investors across Houston, Katy, Sugar Land, and The Woodlands who want to understand how tax rules may affect rental income, property expenses, and long-term financial planning.

In our experience, many real estate owners in Houston are managing properties while also trying to understand how income and expenses are reported for tax purposes. That is when tax strategies often come up. While real estate can offer opportunities for wealth building through appreciation, rental income, and leverage, the tax side of property ownership may feel complex without clear guidance.

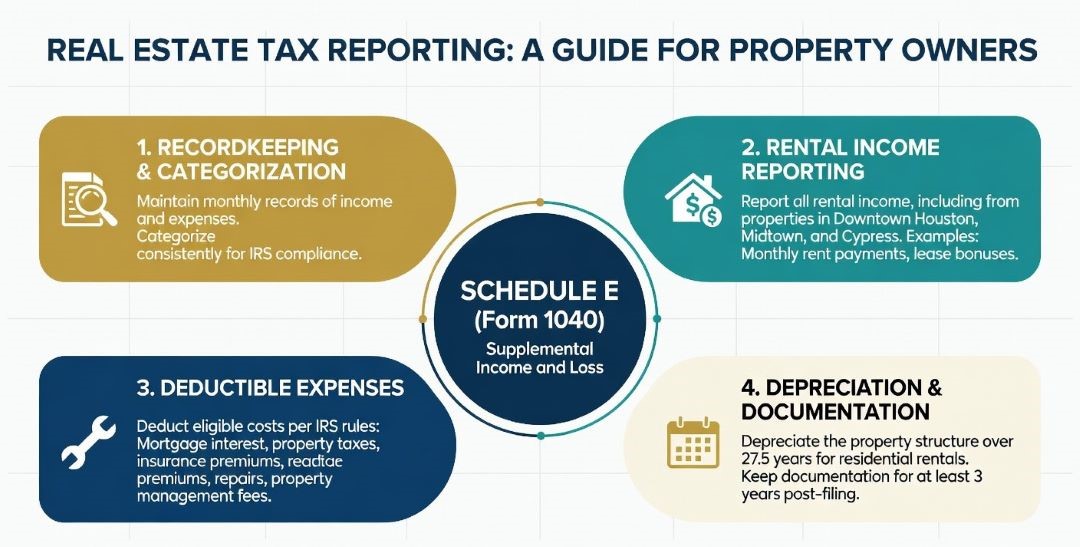

How Real Estate Tax Reporting Generally Works

We often speak with property owners in Downtown Houston, Midtown, and Cypress who are earning rental income but are not sure how to organize records or what expenses may be relevant for tax purposes. In many cases, rental income and expenses are reported on federal tax returns using Schedule E, which is part of the individual income tax filing.

That is one reason real estate tax strategies often start with recordkeeping and consistent categorization. From a tax perspective, rental property owners may be able to report expenses such as mortgage interest, property taxes, insurance, repairs, and property management fees, subject to IRS rules. A few general points often shape the discussion:

- Rental income is generally reportable

- Certain property-related expenses may be deductible

- Depreciation may apply to the property structure

- Documentation and monthly records often matter

For property owners who also operate other businesses or manage contractor payments, bookkeeping & payroll services may support more organized tracking of income and expenses across multiple activities.

What Depreciation Means in a Real Estate Context

One of the most commonly discussed topics when property owners ask about real estate tax strategies is depreciation. Depreciation is a non-cash deduction that generally allows owners to recover the cost of a rental property over a set number of years, subject to IRS guidelines.

In our work with landlords and small property investors in The Heights, West University, and Clear Lake, we often explain that depreciation does not involve an actual cash payment. Instead, it is a deduction that may affect how taxable rental income is calculated over time. The specific recovery period and method can depend on the type of property and how it is used.

According to IRS guidelines, residential rental property is generally depreciated over 27.5 years, while commercial property may follow a different schedule. That guidance may be helpful for Texas property owners who want a high-level view of how depreciation is generally applied.

Why Accurate Recordkeeping Supports Better Tax Reporting

Many property owners tell us they collect rent and pay property expenses throughout the year, but do not track those items consistently. That can create challenges later when it is time to prepare a return or review what expenses may be deductible.

That is another reason real estate tax strategies often begin with better recordkeeping. When records are clearer, it may be easier to prepare accurate tax filings and support reported deductions if questions arise later.

For property owners managing multiple income sources or rental units, business tax preparation may also be relevant, especially when real estate activity is part of a broader business structure or involves contractor payments and vendor expenses.

A Houston Case Study from Recent Client Work

We worked with a property owner in Pearland who had recently purchased a second rental home and was managing both properties while also working a full-time job. As tax season approached, the client asked how rental income and repair costs should be reported and whether there were real estate tax strategies that could help reduce taxable income.

In that type of engagement, we typically review income records, categorize expenses, explain general depreciation concepts, and help the client understand what documentation may be needed to support the return.

How Planning Ahead May Support Long-Term Goals

For many Houston area property owners in Memorial, River Oaks, and Conroe, real estate is not just about current income. It is also part of a longer-term wealth-building approach that may include appreciation, equity growth, and future property sales or exchanges.

From a tax perspective, planning may allow property owners to review timing, expenses, and potential tax considerations ahead of major decisions. For property owners interested in year-round planning support, tax planning may be relevant as part of a broader review of income, deductions, and future goals.

Why Real Estate Tax Rules Can Feel Complex

One reason real estate tax strategies remain a frequent topic is that property ownership often involves multiple tax rules that interact in different ways. Depreciation, passive activity rules, expense categorization, and capital gains treatment all may apply depending on the property and the owner’s broader tax situation.

Property owners may benefit from viewing real estate taxes as part of an ongoing process rather than a one-time event. Keeping better records, reviewing expenses regularly, and planning ahead may all help support clearer tax reporting and better long-term decisions.

FAQs

What are some common real estate tax strategies that property owners review?

Common strategies may include tracking deductible expenses, understanding depreciation, organizing records for rental income, and reviewing timing for property-related decisions. Each property owner’s situation is different.

Can property owners deduct repairs and improvements the same way?

Not always. Repairs that maintain the property may be treated differently from improvements that add value or extend useful life. The IRS generally applies different rules to each category.

Why does recordkeeping matter for rental property taxes?

Clear records may support accurate reporting of income and expenses, help document deductible costs, and make tax preparation easier when filing season arrives.

Is depreciation available for all types of real estate?

In general, depreciation may apply to the building or improvement portion of rental property, but not to the land itself. The specific rules depend on the property type and use.

Conclusion

For property owners across Houston, real estate tax strategies are an important part of managing rental income, property expenses, and long-term wealth-building goals. In our experience, real estate taxes can feel complex, but they become more manageable when supported by organized records and a clear understanding of what expenses and deductions may apply.

A thoughtful approach to recordkeeping and tax planning may help property owners stay organized and make more informed decisions throughout the year. If you’re looking for hands-on support with ongoing financial guidance, Dabney Tax & Accounting Services can provide structured accounting, bookkeeping, and tax support for Houston property owners.