For many high-income earners in Texas, tax planning is an important part of long-term financial management. While traditional investments like stocks or bonds may play a role, the U.S. tax code includes several provisions that can offer oil and gas investment tax benefits to individuals who directly participate in certain energy-related projects. Understanding how these incentives work is an important first step for evaluating whether this type of investment may fit into a broader tax strategy.

As a Houston-based CPA firm, we help clients understand the tax considerations associated with these investments. Direct participation in oil and gas drilling projects can involve significant financial risk, and outcomes vary widely. However, the associated tax provisions are well-established in the tax code and may provide certain deductions for eligible taxpayers, depending on IRS rules and individual circumstances.

Below is an overview of some of the primary tax considerations related to oil and gas investments in 2025.

Why Oil and Gas Tax Incentives?

Congress has long used specific tax provisions to encourage private investment in domestic energy production. These incentives are structured in a way that supports U.S. energy development as outlined in federal tax law.

Because of this policy history, the tax provisions available to eligible investors are not “loopholes” but intentional parts of the tax code designed to support energy-sector participation.

Oil and Gas Investment Tax Benefits of Intangible Drilling Costs (IDC)

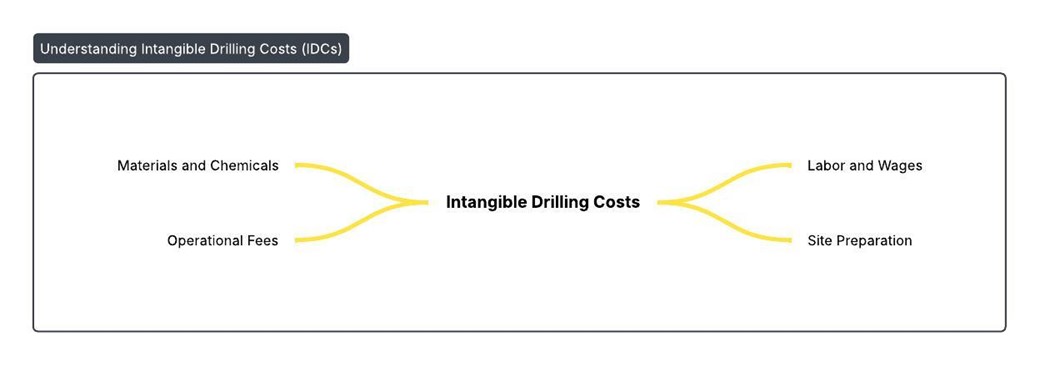

One of the most widely discussed oil and gas investment tax benefits relates to the treatment of Intangible Drilling Costs (IDCs).

What Are Intangible Drilling Costs?

IDCs include the non-salvageable expenses associated with drilling a new well, such as:

- Labor and wages

- Drilling mud, fuel, cement, and chemicals

- Geological work and site preparation

- Hauling and rig-related services

These costs often represent a significant portion of a drilling program’s total budget.

How the IDC Deduction Works

Under the tax code, taxpayers who hold a working interest in an oil or gas well may be able to deduct 100% of their share of IDCs in the year the costs are incurred. This can create a large first-year deduction for eligible investors.

For example, if an investor contributes $100,000 to a drilling project and $80,000 is allocated to IDCs, the investor may be able to deduct the $80,000 allocated to IDCs, depending on participation level and IRS eligibility rules.

How IDC Deductions Help Offset Active Income

One feature of working-interest ownership is that it is generally treated as non-passive activity for tax purposes. As a result, deductions from IDCs may offset active income, such as wages or business income, rather than being limited by passive-loss rules. This is one reason some taxpayers review these provisions with their tax professionals when evaluating participation.

However, whether a taxpayer can use these deductions depends on their individual situation, participation level, and IRS definitions of activity. A detailed consultation with a CPA is essential.

Tangible Drilling Costs (TDCs) and Accelerated Depreciation

The remaining portion of a drilling investment, often 20–40%, is typically allocated to Tangible Drilling Costs. These represent physical assets such as:

- Pumps, casings, and tubing

- Wellheads and tanks

- Other durable equipment

TDCs cannot be deducted immediately but may be depreciated over time, usually across seven years. In some cases, taxpayers may also qualify for accelerated depreciation provisions such as bonus depreciation or Section 179 expensing if applicable. These provisions may increase first-year deductions, depending on eligibility.

The Long-Term Benefit with Percentage Depletion Allowance

Other than the initial deductions, the tax code provides a long-term benefit for productive wells known as the Percentage Depletion allowance. This is one of the long-standing tax provisions applicable to qualifying oil and gas production.

Instead of depreciating the actual cost of the mineral property (cost depletion), the tax code allows independent producers and qualifying taxpayers to deduct 15% of the well’s annual gross income.

One notable aspect of percentage depletion is that total deductions taken over the life of the well are not limited to the original investment. An investor can continue to claim this 15% deduction for as long as the well is producing, meaning the cumulative deduction may exceed the investor’s initial capital outlay, depending on production levels and IRS limits. This allowance is, however, limited to 100% of the net income from the property in any given year.

Working Interest vs. Royalty Interest

To claim these deductions, you must typically invest as a “working interest” owner. Understanding the difference between a working interest and a royalty interest is important when reviewing how tax treatment may apply.

| Feature | Working Interest | Royalty Interest |

| Role | Actively participates in the project | Receives income without participating |

| Costs | Shares in drilling/operating costs | No operating costs |

| IDC Deduction | Generally eligible | Not eligible |

| Passive Loss Rules | Often treated as non-passive | Generally passive |

Understanding this distinction is important when reviewing potential tax treatment.

The Tax Impact of Investing in Oil and Gas Drilling Projects

Consider this simplified scenario:

- Investor: A Houston surgeon with high W-2 income

- Investment: $100,000 in a drilling program in the Permian Basin

- Allocation:

- $80,000 in IDCs

- $20,000 in TDCs

Possible First-Year Tax Treatment

- IDC Deduction: The investor may deduct the $80,000 of IDCs, if eligible.

- TDC Depreciation: If bonus depreciation applies, the investor may deduct the $20,000 for tangible equipment.

- Total Possible Deduction (If Eligible): $100,000

If the well produces income in future years, the investor may also receive revenue distributions and potentially qualify for percentage depletion, depending on eligibility.

This example illustrates how tax provisions may apply but does not represent a guaranteed outcome.

Know the Risks Involved in Oil and Gas Tax Investment

While the oil and gas investment tax benefits can be substantial depending on eligibility and the project’s structure, the underlying investment carries meaningful financial risk. Many wells do not produce at projected levels, and some may not produce at all. These investments are generally considered speculative, and taxpayers should evaluate whether the strategy aligns with their financial capacity and risk tolerance.

Considering These Tax Provisions?

If you are a Texas investor evaluating how oil and gas participation might impact your overall tax picture, the CPA-led team at Dabney Tax & Accounting Services can help you understand the tax rules that may apply to your situation. We do not provide investment advice but can help clarify the tax implications so you can make a more informed decision.

Frequently Asked Questions

1. What is the biggest tax benefit associated with oil and gas investments?

Many investors view the IDC deduction as one of the most notable oil and gas investment tax benefits, because IDCs may be fully deductible in the year incurred. However, eligibility depends on participation rules and the investor’s tax profile.

2. What’s the difference between IDCs and TDCs?

IDCs are non-salvageable costs like labor or fuel; TDCs are physical equipment that is depreciated. IDCs may be deductible immediately, while TDCs follow depreciation rules.

3. Is percentage depletion better than cost depletion?

Percentage depletion may provide larger long-term deductions in some situations, but eligibility and benefits depend on the well’s production and tax rules.

4. What does it mean to have a “working interest”?

A working interest involves participating in the project and sharing in operating costs. Working-interest owners may qualify for certain deductions unavailable to passive royalty owners.

5. Are these tax benefits part of a high-risk strategy?

Oil and gas drilling carries substantial financial risk. The tax provisions can be meaningful, but the underlying investment is speculative and may not produce the financial outcomes the investor anticipates.